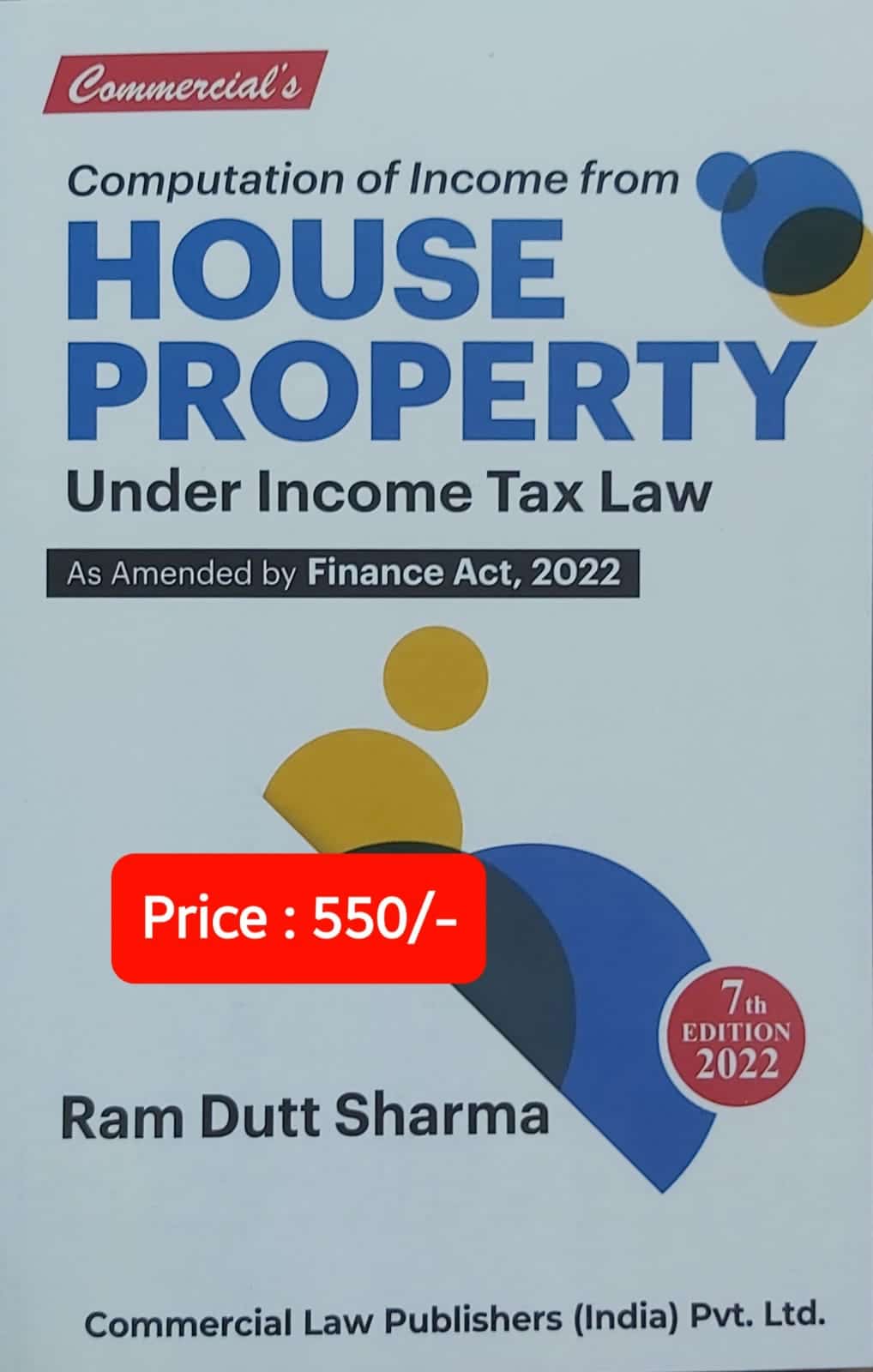

- Publisher : Commercial Law Publishers (India) Pvt. Ltd.

- Author : Ram Dutt Sharma

- Edition : 7th Edition 2022

- ISBN-13 : 9789356030541

- ISBN-10 : 9789356030541

- Language : English

- Binding : Paperback

Commercial’s Computation of Income From House Property by Ram Dutt Sharma – 7th Edition 2022.

Commercial’s Computation of Income From House Property by Ram Dutt Sharma – 7th Edition 2022.

About the book

Income from house property’ is one of the five heads of income chargeable to tax under the Income-tax Act, 1961 (‘the Act’), Section 22 of the Act is the charging section and section 23 defines the ‘annual value of the house property which is charged to tax. Section 24 allows certain deductions out of the annual value’ computed in accordance with the provisions of section 23, Section 25 deals with those amounts which are inadmissible. Sections 25A and 25AA deal with the tax treatment of ‘unrealised rent’ and section 25B deals with the ‘arrears of rent received’. Section 26 refers to the property owned by co-owners and section 27 discusses the cases of ‘deemed ownership’ where the owner is not the actual owner of the property. From these provisions, important concepts of ‘annual value’, ‘property consisting of building or land appurtenant thereto’, ownership, unrealized rent and recovery thereof, self occupied property in certain cases, etc., emerge.

This book deals with the income charged under the head “Income from House Property”. Any buildings or lands appurtenant thereto, of which the as sessee is owner, is chargeable to tax under the head “Income from House Property”. The scope of income charged under this head is defined by section 22 of the Income Tax Act and the computation of income falling under this head is governed by sections 23 to 27 Tax levied under section 22 is tax on annual value of house property and it is not a tax on house property. “Income from House Property” is the only head under the Act which is charged on “Notional basis” instead of real income.

In this book, I have summarised and explained the provisions in the Income-tax Act, 1961 relating to computation of income from house property. I have explained the provisions almost chronologically, starting with the basic conditions to be satisfied, and then proceed to the actual computation including permissible deductions.

All the provisions relating to tax treatment of income from house property are explained in this book. It is an attempt to provide answers to common queries on income under the head House Property in a very simple language. The book aims to provide solutions for house property owner’s day to-day problems and contains many chapters. The subject has been arranged in a very systematic manner beginning with an introduction chapter about Income from House Property and then discussing exempted income from house property.

Another chapter has been devoted to an exclusive chapter written on “Deemed owners of the house property” discussing the deemed owner of house property who is also chargeable to tax under the head “Income from house property”. Next few chapters are devoted to Treatment of Composite Rent, Set off & carry forward of loss, Tax Deduction at source from Rent, House Property income of Non-Resident Indians (NRIs) in India.

Each chapter provides the introduction, conditions and quantum of exemptions/deductions available and other requirements to be fulfilled. In the end chapter such as selected case laws have been provided for a ready reference.

I have also covered some relevant case law, and has also touched upon allied issues such as treatment of losses and computation of Income from house property. This book has been prepared to help taxpayers in discharging their obligations in respect of income from house property. After going through this book, I am sure everyone will be able to understand the meaning and computation of Income from House Property. The amendments made by the Finance Act have been incorporated at appropriate places in this book.

I also wish this publication will also be a comprehensive aid to the readers for understanding the complex law of computation of income from house property and receive widespread patronage.

I would like to place on record a special note of gratitude to Sh. Ashok Kumar Manchanda, IRS (1976- Batch) who has been the guiding force and a constant source of inspiration in my life. I also express my thanks to Commercial Law Publishers (India) Pvt Ltd. who reposed confidence in me and published Fourth Edition of this book. As usual, they have done a good job in making this volume attractive, acceptable and useful.

Although, every effort has been made to support every information given in the book with the relevant sections and the rules of law, however, the book should not be construed as an exhaustive statement of law. The relevant provisions of the Income Tax Act and the Income Tax Rules, may be referred to, if necessary.

Though every care has been taken to provide authentic information yet the author/publisher are not legally or morally responsible for any loss or damage that may arise to any person from any inadvertent error or omission in the book. I however, always welcome suggestions and criticism from esteemed readers for further improvement of the future editions of the book.

Details :-

| Publisher | |

|---|---|

| Author | |

| Language |

Be the first to review “Commercial’s Computation of Income From House Property by Ram Dutt Sharma – 7th Edition 2022”

Related products

15% Off

Original price was: ₹2,995.00.₹2,546.00Current price is: ₹2,546.00.

20% Off

Original price was: ₹1,195.00.₹956.00Current price is: ₹956.00.

25% Off

Original price was: ₹995.00.₹746.00Current price is: ₹746.00.

25% Off

GST

Bharat’s How to handle GST Audit with real life case studies by CA. Arun Chhajer – 1st Edition 2023

Original price was: ₹695.00.₹521.00Current price is: ₹521.00.

25% Off

Original price was: ₹2,875.00.₹2,156.00Current price is: ₹2,156.00.

15% Off

Original price was: ₹2,995.00.₹2,546.00Current price is: ₹2,546.00.

25% Off

Original price was: ₹2,375.00.₹1,781.00Current price is: ₹1,781.00.

17% Off

Original price was: ₹3,995.00.₹3,316.00Current price is: ₹3,316.00.

Reviews

There are no reviews yet.