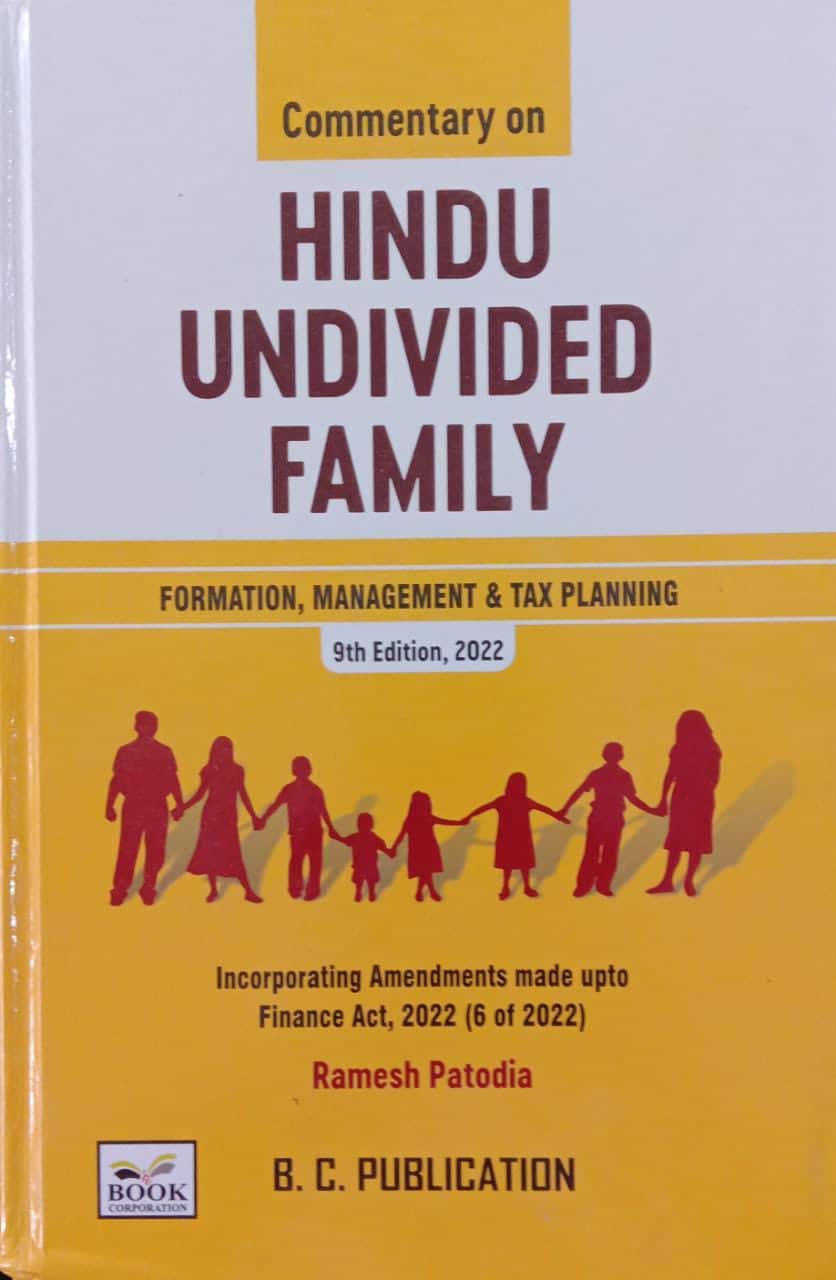

Book Corporation’s Commentary on Hindu Undivided Family by Ramesh Patodia – 9th Edition 2022

Original price was: ₹1,297.00.₹973.00Current price is: ₹973.00.

Book Corporation’s Commentary on Hindu Undivided Family – Formation, Management & Tax Planning by Ramesh Patodia – 9th Edition 2022.

10 in stock

Book Corporation’s Commentary on Hindu Undivided Family – Formation, Management & Tax Planning by Ramesh Patodia – 9th Edition 2022.

Book Corporation’s Commentary on Hindu Undivided Family – Formation, Management & Tax Planning by Ramesh Patodia – 9th Edition 2022.

Details :-

Book Corporation’s Commentary on Hindu Undivided Family – Formation, Management & Tax Planning by Ramesh Patodia – 9th Edition 2022.

Commentary on HINDU UNDIVIDED FAMILY FORMATION, MANAGEMENT & TAX PLANNING Covering the legal issues relating to HUF and Including threadbare analysis regarding applicability of amendment made by the Hindu Succession (Amendment) Act, 2005 to Law relating to Married, unmarried daughters and daughter in law.

Incorporating Amendments made upto Finance Act, 2022 (6 of 2022).

Preface to the Ninth Edition

The last edition of the book was published in the year 2014 in the aftermath of amendment made to the Hindu Succession Act, 1956 by the amending Act of 2005 when the rights of daughters were recognised by the law. However, inspite of such amendment, it was not until the year 2020 when such amendments were interpreted in the case of Vineeta Sharma vs Rakesh Sharma & Ors (2020) 9 SCC 1(SC) by three judges bench of the Supreme Court of India on 11th August 2020 when Hon’ble Justice Arun Mishra writing on behalf of himself and his brother judges clarified that the amended law was applicable to all daughters whether married or born on or before the date of amendment made in the year 2005 or after that date by overruling the earlier decision of Supreme Court in the case of Prakash & Ors vs Phulavati & Ors. (2016) 2 SCC 36 (SC) Thus, the law now can be said to be settled in this regard. It is also now clear that the female can act as a Karta of HUF and it is not necessary for a Joint Hindu Family either under the Hindu Law or under the Income tax Act,1961 to have male child in order to be constituted validly.

The books also deals with the controversy which had been existing regarding the deemed dividend u/s 2(22)(e) of the Income-tax Act,1961 when the Karta was the registered shareholder but the beneficial ownership was with the HUF and which has since been clarified by the Supreme Court in the case of Gopal and Sons (HUF) vs CIT, Kolkata-XI (2017) 3 SCC 574(SC).

On 19 April, 2022 the Supreme Court in the case of K.C. Laxmana vs K.C. Chandrappa Gowda & Anr 2022 Live Law (SC) 381 laid down important law regarding the powers of Karta regarding gift/alienation of the HUF property and the same has been discussed in this book.

The present edition thus takes into account the effect of all these decisions and pronouncements. The book also deals with the amendments as well as other changes which have been made in these years under the Income-tax Act, 1961 primarily and other laws that effect the manner in which the HUFs are governed and function ng within the frame work of law.

The book has incorporated the various important Law Commission Reports also which have dealt with the Hindu Law in detail. One issue which is now before the Supreme Court regarding challenge to Section 15 of the Hindu Succession Act, 1956 as being discriminatory has also been dealt with.

Details :

- Publisher: Book Corporation

- Author : Ramesh Patodia

- Edition : 9th Edition 2022

- Language: English

- ISBN-10 : 8906077413410

- ISBN-13 : 8906077413410

| Author | |

|---|---|

| Language | |

| Publisher |

Be the first to review “Book Corporation’s Commentary on Hindu Undivided Family by Ramesh Patodia – 9th Edition 2022”

Related products

Reviews

There are no reviews yet.