- Binding : Paperback

- Publisher : Taxmann

- Author : Srinivasan Anand G

- Edition : September 2024

- Language : English

- ISBN-10 : 9789364556439

- ISBN-13 : 9789364556439

20% Off

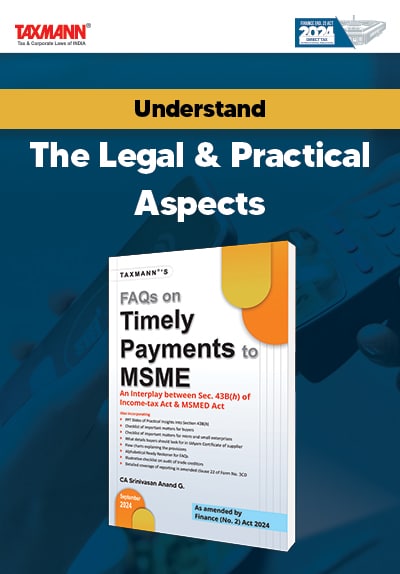

Taxmann’s FAQs on Timely Payments to MSME by Srinivasan Anand G – Edition September 2024

Original price was: ₹445.00.₹356.00Current price is: ₹356.00.

Taxmann’s FAQs on Timely Payments to MSME – An Interplay between Sec. 43B(h) of the Income-tax Act & MSMED Act by Srinivasan Anand G – Edition September 2024. This book provides a detailed guide on ensuring timely payments to MSMEs, emphasising Section 43B(h) of the Income-Tax Act, 1961, and the MSMED Act, 2006. The key features include in-depth analyses of legal provisions, buyer obligations, and the impact of the non-obstante clause. It provides practical FAQs, compliance checklists, and accounting and reporting requirements guidance.

9 in stock

Taxmann’s FAQs on Timely Payments to MSME – An Interplay between Sec. 43B(h) of the Income-tax Act & MSMED Act by Srinivasan Anand G – Edition September 2024.

Taxmann’s FAQs on Timely Payments to MSME – An Interplay between Sec. 43B(h) of the Income-tax Act & MSMED Act by Srinivasan Anand G – Edition September 2024.

Description

This book is a comprehensive guide to ensuring timely payments to Micro, Small, and Medium Enterprises (MSMEs), focusing on Section 43B(h) of the Income-Tax Act, 1961, and its interplay with the MSMED Act, 2006. It provides frequently asked questions, offering:

- Clarity on Legal Provisions

- Rationale Behind the Laws

- Implications for Businesses

This guidebook is designed for legal professionals, accountants, business owners, and anyone involved in transactions with MSMEs, providing analysis for legal compliance for timely payments and the broader implications for business practices.

The Present Publication is the September 2024 Edition, authored by CA. Srinivasan Anand G. This book is amended by the Finance (No. 2) Act, 2024 with the following noteworthy features:

- Detailed Analysis of Provisions

- In-depth examination of Section 43B(h) of the Income Tax Act, 1961

- Analysis of deductions related to payments to MSMEs

- Impact of the non-obstante clause on other sections of the Income Tax Act and its implications for accounting methods and capital goods purchases

- Discussion on the conditions under which deductions are allowed or disallowed, emphasising the timing of payments

- Application to Various Buyers

- Identification of types of buyers affected by Section 43B(h)

- Consideration of scenarios involving charitable trusts, entities under presumptive taxation schemes, and different accounting methods

- Evaluation of Udyam-registered MSMEs as buyers and their obligations

- Definitions and Classifications

- Clarification of the terms’ micro enterprise’ and ‘small enterprise’

- Criteria for classification based on turnover and investment

- Guidance on verifying the status of suppliers and the authenticity of Udyam Registration numbers

- Implications for tax benefits based on enterprise classification

- Compliance Under the MSMED Act

- Explanation of buyers’ obligations to make timely payments as mandated by Section 15 of the MSMED Act

- Calculation of due dates, definition of ‘supplier’, and consequences of non-compliance

- Legal requirements for interest on delayed payments and methods of calculation

- Accounting and Reporting Requirements

- Extensive discussion on the accounting treatment of amounts due to MSEs

- Disclosure requirements in audited accounts and the tax audit report

- Highlighting common errors with checklists for compliance for buyer entities and MSEs

- Illustrative Checklist on Audit of Trade Creditors

- Includes a practical checklist for auditing trade creditors under Section 44AB, focusing on Clause 22 and Section 43B(h) requirements

- Practical Scenarios and Examples

- FAQs addressing real-life scenarios, such as the impact of advance payments and the handling of retention money

- Advice on dealing with payments made beyond prescribed time frames

- Practical guidance for navigating compliance complexities with Section 43B(h)

The detailed contents of this book are as follows:

- [Objects and Rationale of Section 43B(h)] – The chapter introduces Section 43B(h) of the Income-Tax Act, explaining its objectives, historical context, and the necessity for its enactment alongside the MSMED Act’s Chapter V. It clarifies the section’s aims to ensure prompt financial transactions with MSMEs and the legal consequences of delayed payments

- [Provisions of Section 43B(h)] – Detailed analysis of what Section 43B(h) entails, including deduction criteria for payments to MSMEs, the significance of the non-obstante clause, and the impact on other sections of the Income-Tax Act. It also discusses specific scenarios, such as payments for capital goods, advance payments, and implications of delayed payments within and beyond financial years

- [Applicability to Buyers] – Identifies the types of buyers to whom Section 43B(h) applies, including charitable trusts, entities opting for presumptive taxation schemes, and Udyam-registered MSMEs. It explores various scenarios to determine the applicability of the section

- [Definitions and Classifications] – Explains the definitions of ‘micro-enterprise’ and ‘small enterprise’, the criteria for classification based on turnover and investment, and the process of determining an enterprise’s classification through financial documents and registration details

- [Liability Under MSMED Act] – Elaborates on the obligations of buyers under Section 15 of the MSMED Act for making timely payments, the calculation of due dates, and the legal definition of terms like ‘the appointed day’, ‘the day of acceptance’, and ‘the day of deemed acceptance’

- [Computation of Disallowance under Section 43B(h)] – Discusses the method of calculating disallowance for late payments, including considerations of net amount, impact of Section 145A, and the specific computation for book profits

- [Disallowance and Interest on Delayed Payments] – Covers the computation of interest on delayed payments as per Section 16 of the MSMED Act, the applicability of interest despite contractual terms, and the tax treatment of such interest

- [Disclosures and Reporting Requirements] – Details the requirements for disclosing amounts due to MSEs in audited accounts, objectives behind these disclosures, identification of MSE suppliers for compliance, and penalties for non-disclosure

- [Tax Audit Reporting of Disallowance under Section 43B(h)] – Specifies the requirement for reporting disallowance under Section 43B(h) in the tax audit report Form No. 3CD

- [Checklists for Compliance] – Provides checklists for buyer entities and micro/small enterprises to ensure adherence to provisions against delayed payments under Section 43B(h) and the MSMED Act.

Details

| Publisher | |

|---|---|

| Language | |

| Author |

Be the first to review “Taxmann’s FAQs on Timely Payments to MSME by Srinivasan Anand G – Edition September 2024”

Related products

25% Off

Original price was: ₹1,995.00.₹1,496.00Current price is: ₹1,496.00.

25% Off

Original price was: ₹799.00.₹599.00Current price is: ₹599.00.

17% Off

Original price was: ₹3,995.00.₹3,316.00Current price is: ₹3,316.00.

25% Off

Original price was: ₹750.00.₹563.00Current price is: ₹563.00.

25% Off

GST

Bharat’s How to handle GST Audit with real life case studies by CA. Arun Chhajer – 1st Edition 2023

Original price was: ₹695.00.₹521.00Current price is: ₹521.00.

25% Off

Income Tax

Commercial’s Filing of Indian Income Tax Updated Return by Ram Dutt Sharma – Edition 2023

Original price was: ₹295.00.₹221.00Current price is: ₹221.00.

25% Off

Original price was: ₹2,695.00.₹2,021.00Current price is: ₹2,021.00.

Reviews

There are no reviews yet.