- Binding : Softcover

- Publisher : Taxmann

- Author : All India Federation of Tax Practitioners

- Edition : 1st Edition 2025

- Language : English

- ISBN-10 : 9789364555821

- ISBN-13 : 9789364555821

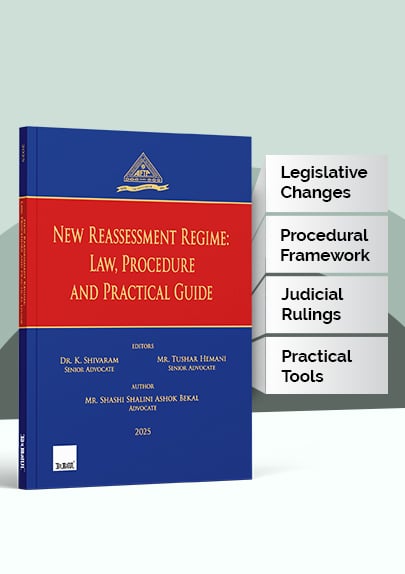

Taxmann’s New Reassessment Regime – Law | Procedure | Practical Guide by AIFTP

₹1,395.00

Taxmann’s New Reassessment Regime – Law | Procedure | Practical Guide by AIFTP – Edition 2025. This book offers an in-depth analysis of the reassessment provisions under the Income-tax Act, 1961. It comprehensively covers critical legislative changes, including Section 148A inquiries, faceless reassessment procedures, and revised timelines for reopening cases. The book discusses key judicial rulings, penalties, prosecution, and writ remedies while providing practical compliance tools such as checklists, templates, and step-by-step guidance. With its meticulous analysis of legislative amendments, procedural frameworks, and curated CBDT instructions, this publication is an indispensable guide for tax professionals, legal practitioners, and policymakers navigating the complexities of the reassessment regime.

10 in stock

Taxmann’s New Reassessment Regime – Law | Procedure | Practical Guide by AIFTP – Edition 2025.

Taxmann’s New Reassessment Regime – Law | Procedure | Practical Guide by AIFTP – Edition 2025.

Description

This book is an authoritative resource on the overhauled reassessment provisions under the Income-tax Act, 1961, as amended by the Finance Act, 2021, and Finance (No. 2) Act, 2024. It analyses the procedural changes, including Section 148A inquiries, revised timelines, and faceless reassessment, while providing historical context and understanding of key judicial rulings such as Union of India v. Ashish Agarwal [2022] 138 taxmann.com 64 (SC). It offers practical tools, checklists, and guidance to simplify the complexities of reassessment.

The book is helpful for tax professionals, legal practitioners, and policymakers seeking clarity on the revamped reassessment framework.

The Present Publication is the 1st Edition, edited by Dr K. Shivaram and Mr Tushar Hemani (Senior Advocate) and authored by Mr Shashi Bekal (Advocate). The noteworthy features of the book are as follows:

- [Comprehensive Analysis of Legislative Changes] The book explains the significant amendments brought by the Finance Act, 2021 and the Finance (No. 2) Act, 2024. It covers the shift from the “reason to believe” doctrine to pre-notice inquiries under Section 148A, revised timelines for reassessment, and the introduction of faceless reassessment procedures

- [Judicial Rulings and Case Law Analysis] It incorporates detailed discussions on landmark judicial decisions, including Union of India v. Ashish Agarwal [2022] 138 taxmann.com 64 (SC) and Union of India v. Rajeev Bansal [2024] 167 taxmann.com 70 (SC), to illustrate the impact of courts on the evolving reassessment provisions. These cases highlight procedural safeguards, interpretations, and the judiciary’s role in shaping the reassessment framework

- [Historical Context and Evolution] Tracing the reassessment regime from its origins under the Income-tax Act, 1922, the book provides a historical perspective that contextualises the recent changes within the broader evolution of tax law in India

- [Practical Guidance for Compliance] The book offers hands-on tools, including detailed checklists, step-by-step guidance for responding to reassessment notices, and practical tips for ensuring procedural compliance. It simplifies complex procedures for easy implementation

- [Discussion on Penalties and Prosecution] It analyses penalties and prosecution provisions related to reassessment, offering clarity on compliance requirements, potential liabilities, and how to address common pitfalls

- [Analyses of Writ Remedies] It provides a detailed discussion on writ jurisdictions and remedies, outlining the constitutional avenues available to taxpayers to challenge reassessment notices and orders

- [CBDT Instructions and Standard Operating Procedures (SOPs)] The book features curated annexures containing relevant CBDT notifications, instructions, and SOPs, offering a ready reference for professionals dealing with reassessment cases

- [Simplified Language and Accessibility] Written in clear and concise language, the book bridges the gap between technical legal provisions and practical application, making complex topics accessible to readers

- [Broad Scope of Coverage] Topics include timelines for reopening assessments, faceless reassessment, appellate mechanisms, writ petitions, penalties, and recent procedural changes, ensuring a holistic understanding of the reassessment process

The book is methodically structured to provide an in-depth understanding of reassessment provisions under the Income-tax Act, 1961, combining historical context, legislative changes, judicial interpretations, and practical guidance.

- Introduction and Historical Context

- Overview of reassessment provisions and their evolution from the Income-tax Act, 1922

- Contextual analysis of how reassessment has shaped tax law over decades

- Legislative Changes

- Detailed coverage of the Finance Act, 2021, and Finance (No. 2) Act, 2024

- Key amendments such as Section 148A, faceless reassessment, and updated timelines for reopening cases

- Judicial Interpretations

- Landmark cases like UOI v. Ashish Agarwal and UOI v. Rajeev Bansal

- Role of courts in shaping reassessment procedures and ensuring procedural fairness

- Key Provisions and Concepts

- A Comprehensive exploration of Sections 147 to 153

- Explanation of terms like income escaping assessment, procedural safeguards, and conditions for reopening cases

- Practical Tools and Procedural Guidance

- Step-by-step instructions for responding to notices and preparing effective representations

- Practical checklists for compliance and navigating procedural complexities

- Faceless Reassessment and CBDT Guidance

- Explanation of faceless reassessment procedures and their implications

- Compilation of relevant CBDT instructions, standard operating procedures, and notifications

- Special Topics and Challenges

- Penalties, prosecution, and their implications under the reassessment regime

- Discussion of constitutional remedies, writ petitions, and appellate mechanisms available to taxpayers

- Case Studies and Examples

- Practical examples and curated case studies to demonstrate the application of reassessment provisions

- Annexures and Reference Material

- Statutory references, CBDT guidelines, and procedural clarifications

- Comprehensive subject index and list of cases for easy navigation

Details

| Language | |

|---|---|

| Publisher | |

| Author |

Be the first to review “Taxmann’s New Reassessment Regime – Law | Procedure | Practical Guide by AIFTP”

Related products

15% Off

Original price was: ₹2,995.00.₹2,546.00Current price is: ₹2,546.00.

25% Off

GST

Bharat’s How to handle GST Audit with real life case studies by CA. Arun Chhajer – 1st Edition 2023

Original price was: ₹695.00.₹521.00Current price is: ₹521.00.

25% Off

Original price was: ₹15,000.00.₹11,250.00Current price is: ₹11,250.00.

20% Off

Original price was: ₹1,195.00.₹956.00Current price is: ₹956.00.

25% Off

Original price was: ₹750.00.₹563.00Current price is: ₹563.00.

25% Off

Original price was: ₹799.00.₹599.00Current price is: ₹599.00.

25% Off

MSME

Bloomsbury’s Treatise on Micro, Small and Medium Enterprises by Rajeev Babel – 1st Edition June 2021

Original price was: ₹1,799.00.₹1,349.00Current price is: ₹1,349.00.

25% Off

Original price was: ₹2,375.00.₹1,781.00Current price is: ₹1,781.00.

Reviews

There are no reviews yet.